A record 3,834 Medicare Advantage plans will be available across the country as alternatives to traditional Medicare for 2022, a new KFF analysis finds. That’s an increase of 8 percent from 2021, and the largest number of plans available in more than a decade.

At the same time, the number of Medicare Part D stand-alone prescription drug plans that will be offered in 2022 is decreasing by 23 percent to 766 plans, primarily the result of firm consolidations leading to fewer plan offerings sponsored by Cigna and Centene, according to another new KFF analysis.

These findings are featured in two briefs released by KFF today that provide an overview of the Medicare Advantage and Medicare Part D marketplace for 2022, including the latest data and key trends over time. Medicare’s open enrollment period began Oct. 15 and runs through Dec. 7.

Medicare Advantage

More than 26 million Medicare beneficiaries – 42 percent of all beneficiaries – are currently in Medicare Advantage plans, which are mostly HMOs and PPOs offered by private insurers that are paid to provide Medicare benefits to enrollees.

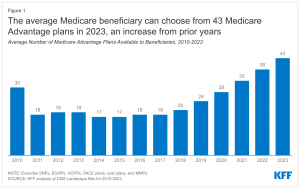

In 2022, a typical beneficiary will have 39 plans to choose from in their local market. But the number of Medicare Advantage plans available varies greatly across the country, with an average of 42 plans in metropolitan areas and 25 plans in non-metropolitan areas. In 2022, 25 percent of beneficiaries live in a county where they can choose among 50 Medicare Advantage plans.

Most Medicare Advantage plans (89%) include prescription drug coverage. Fifty-nine percent of these plans do not charge any additional premium beyond Medicare’s standard Part B premium. More than 90 percent of non-group Medicare Advantage plans offer some vision, telehealth, hearing, or dental benefits.

Despite the average beneficiary having access to plans offered by nine different firms, Medicare Advantage enrollment is concentrated in plans operated by UnitedHealthcare, Humana, and Blue Cross Blue Shield affiliates. Together, UnitedHealth and Humana account for 45 percent of Medicare Advantage enrollment in 2021.

Part D

As a result of consolidations in the stand-alone drug plan market, the typical Medicare beneficiary will have a choice of 23 stand-alone drug plans next year, seven fewer than in 2021. Beneficiaries receiving low-income subsidies (LIS) will also have fewer premium-free plan choices in 2022, which could make it more difficult for some enrollees to find a premium-free plan that covers all their prescription medications. In the stand-alone drug plan market, 8 out of 10 enrollees next year are projected to be in stand-alone plans operated by just four firms: CVS Health, Centene, UnitedHealth, and Humana.

The estimated average monthly premium for Medicare Part D stand-alone drug plans is projected to be $43 in 2022, based on current enrollment, while average monthly premiums for the 16 national stand-alone drug plans available in 2022 are projected to range from $7 to $99.

Nearly three-fourths, or 10 million, of the 13.3 million stand-alone drug plan enrollees who don’t qualify for low-income subsidies will have to pay higher premiums next year if they stick with their current plan, and many will also face higher deductibles and cost sharing for covered drugs. While the average weighted monthly PDP premium is increasing by $5 between 2021 and 2022 (from $38 to $43), nearly 4 million non-LIS enrollees (28%) will see a premium increase of $10 or more per month. Substantially fewer non-LIS enrollees (0.2 million, or 2%) will see a premium reduction of the same magnitude.

In addition to these two new analyses, KFF has updated its collection of frequently asked questions about Medicare Open Enrollment to help beneficiaries understand their options during the annual open enrollment period. A recent KFF analysis found that 7 in 10 Medicare beneficiaries say they did not compare their options during a recent open enrollment period. Comparing and choosing among the wide array of Part D plans can be difficult, given that plans differ from each other in multiple ways, beyond premiums, including cost sharing, deductibles, covered drugs, and pharmacy networks. Comparing Medicare Advantage drug plans may be made more difficult by the fact that not only drug coverage varies but also other features, including cost sharing for medical benefits, provider networks, and coverage and costs for supplemental benefits.